Credit: GRI Club

Credit: GRI Club Can France revive itself and face the challenges of 2024?

France’s biggest RE voices met to discuss market trends, with Hélène Baudchon and Olivier Ambrosiali, BNP Paribas

January 31, 2024Real Estate

Written by Helen Richards

Can France revive itself and face the challenges of 2024? This was the question among real estate investors, lenders, asset managers, and economists gathered at GRI Club’s first economic forum of 2024, Coup d’envoi du marché immobilier 2024, in Paris.

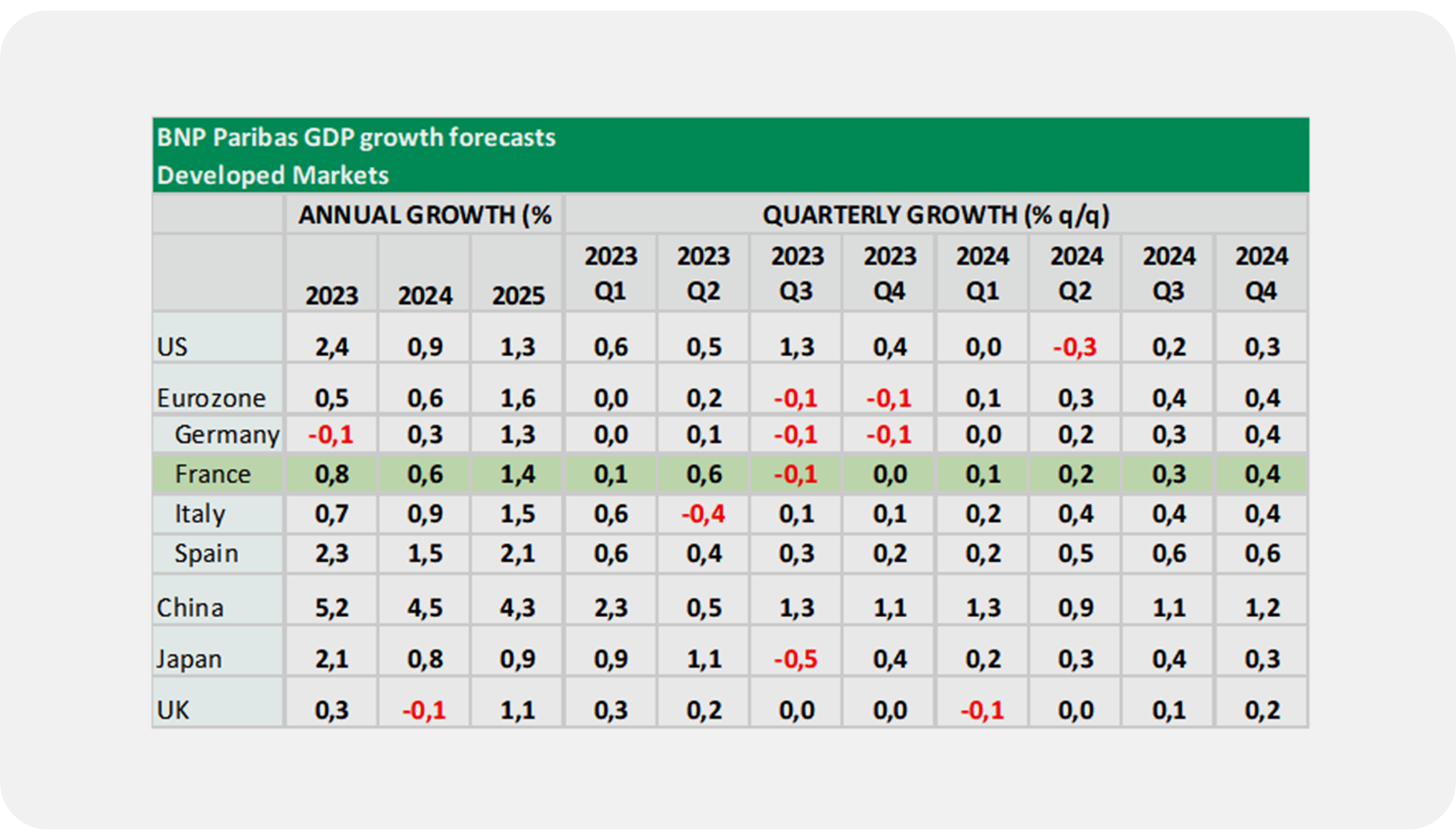

France, similar to the rest of the eurozone, is on the verge of recession with zero to slightly negative growth expected in Q4 2023, and zero to barely positive growth in Q1 2024. A modest recovery is expected from spring, prompted more by household consumption than by companies.

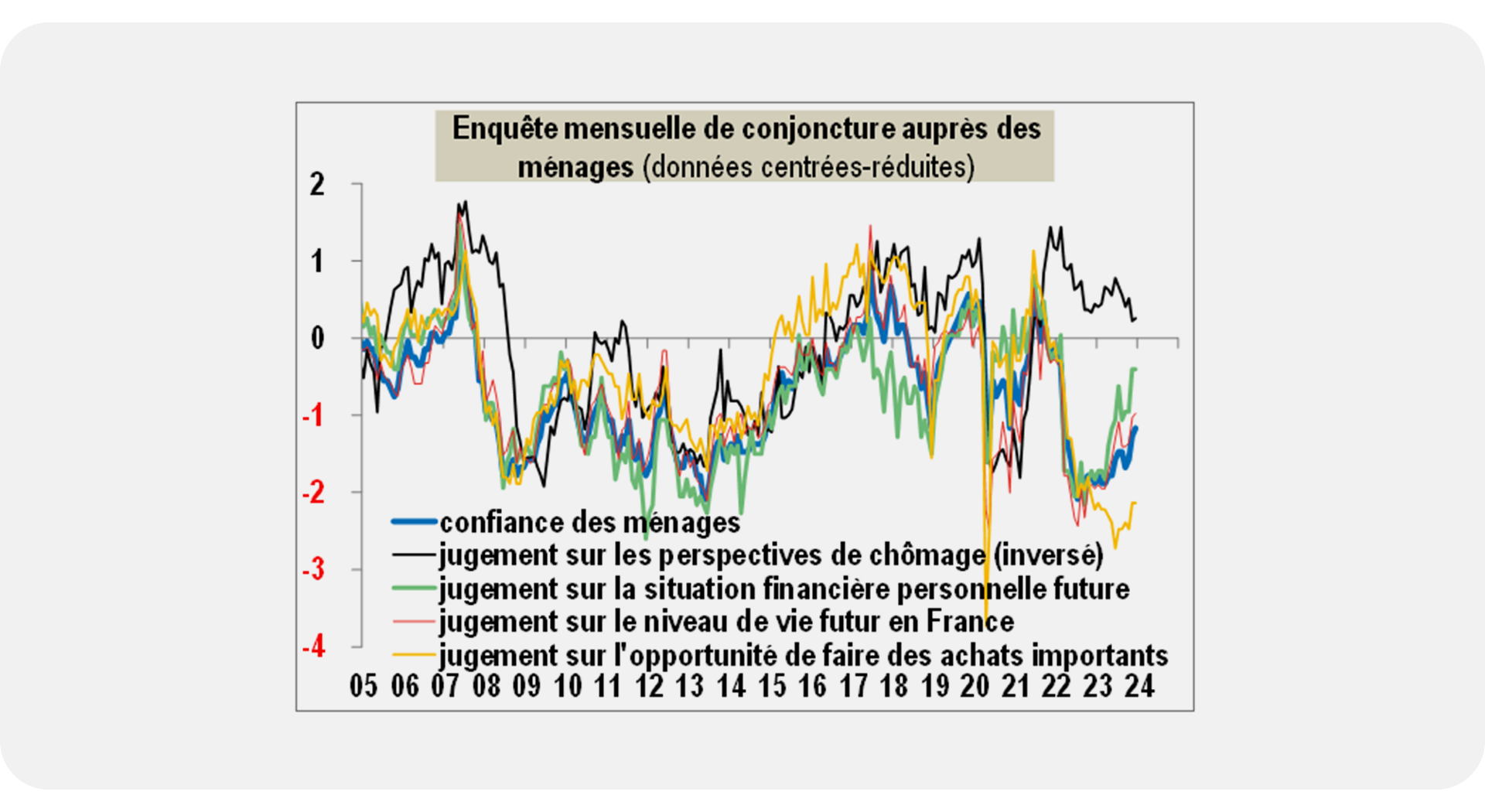

PMIs (Purchasing Managers' Index) and the ESI (economic sentiment indicator) in the eurozone are slightly encouraging, having both shown recent increases. Meanwhile, recent surveys show mixed sentiments from the French population regarding unemployment prospects, personal finance, standard of living, and chances of making major purchases. Monthly household survey results in France since 2005 (scaled data) (Image: INSEE, Macrobond, BNP Paribas)

Monthly household survey results in France since 2005 (scaled data) (Image: INSEE, Macrobond, BNP Paribas)

The country is experiencing ongoing disinflation, which is expected to continue until falling below the 2% target around summer. This is an important factor supporting growth, as is wage growth, which, although weaker than in 2023, should remain dynamic.

The situation on the labour market is becoming less favourable, although the expected rise in unemployment should remain contained. The substantial rise in defaults also constitutes a significant downside risk to the labour market.

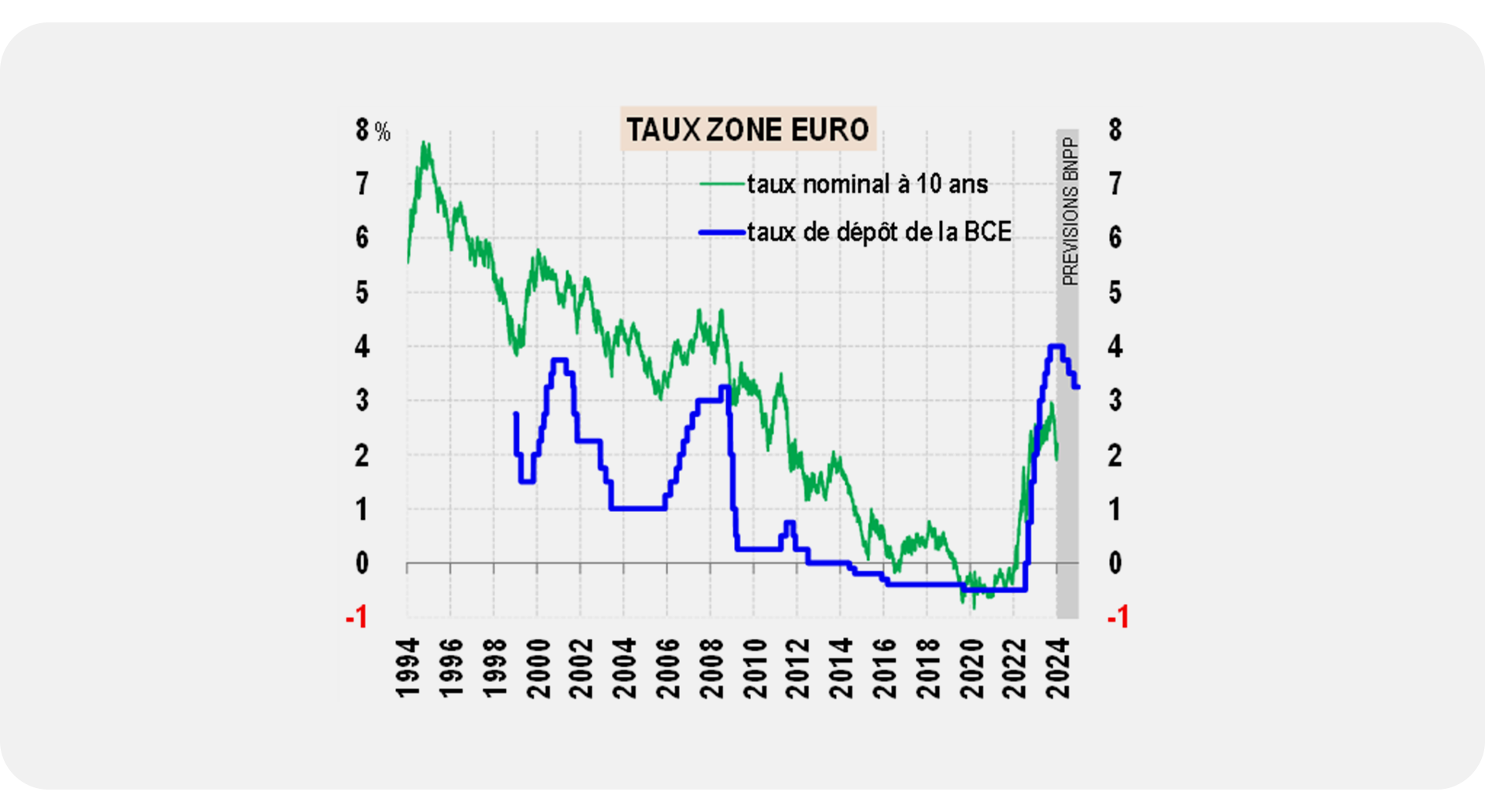

The adverse effects from previous interest rate hikes may not have been fully felt yet. In fact, both negative and positive effects are still to be felt. The expected and observed decreases in central interest rates, which influence long-term interest rates, are already yielding positive results.

The housing crisis is expected to continue, running the risk of impacting the wider economy. Other challenges faced by the market include ensuring fiscal stability, trade-competitiveness deficit, and transaction volumes.

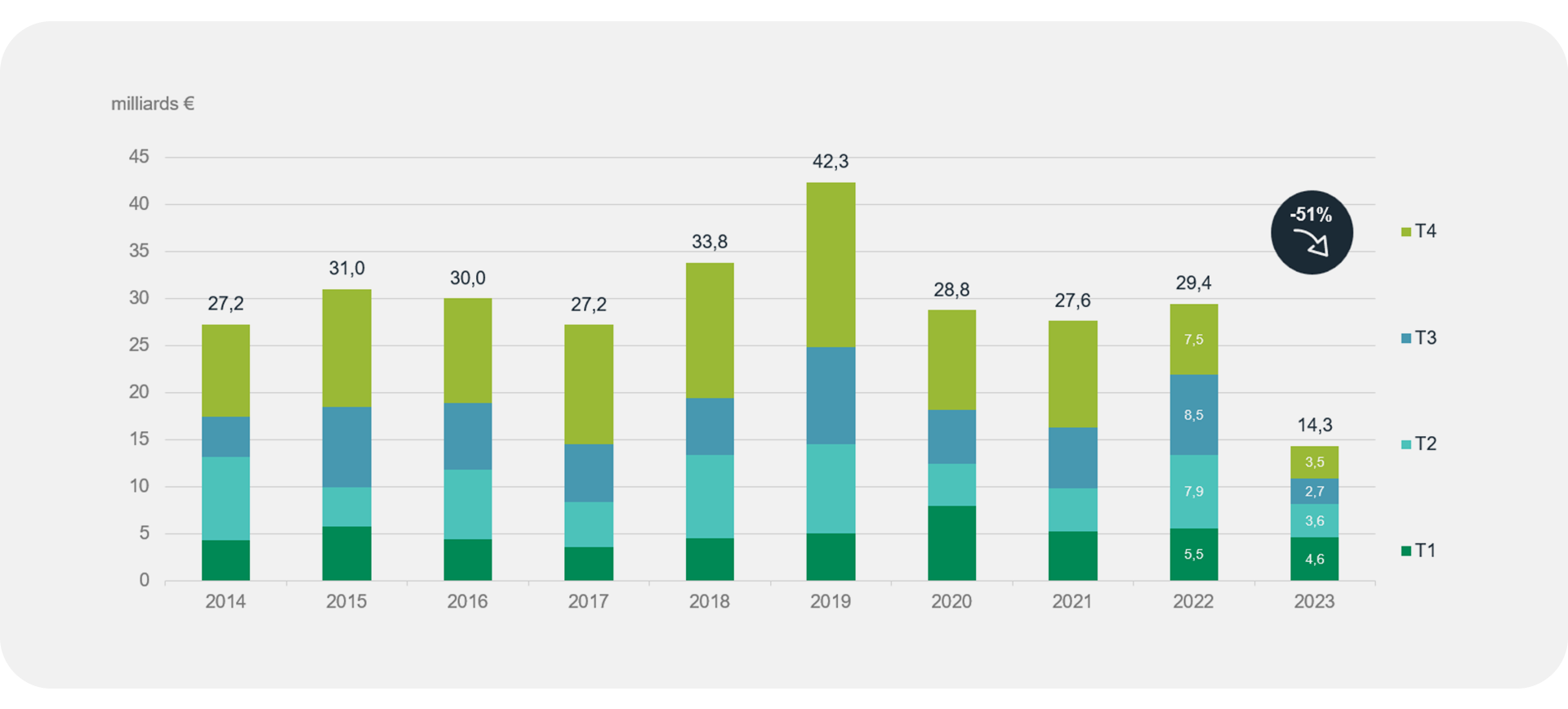

Last year, France saw a considerably lower level of real estate investment, with a total of approximately 14 billion euros, compared with an annual investment of around 28 to 29 billion euros annually between 2020 and 2022.

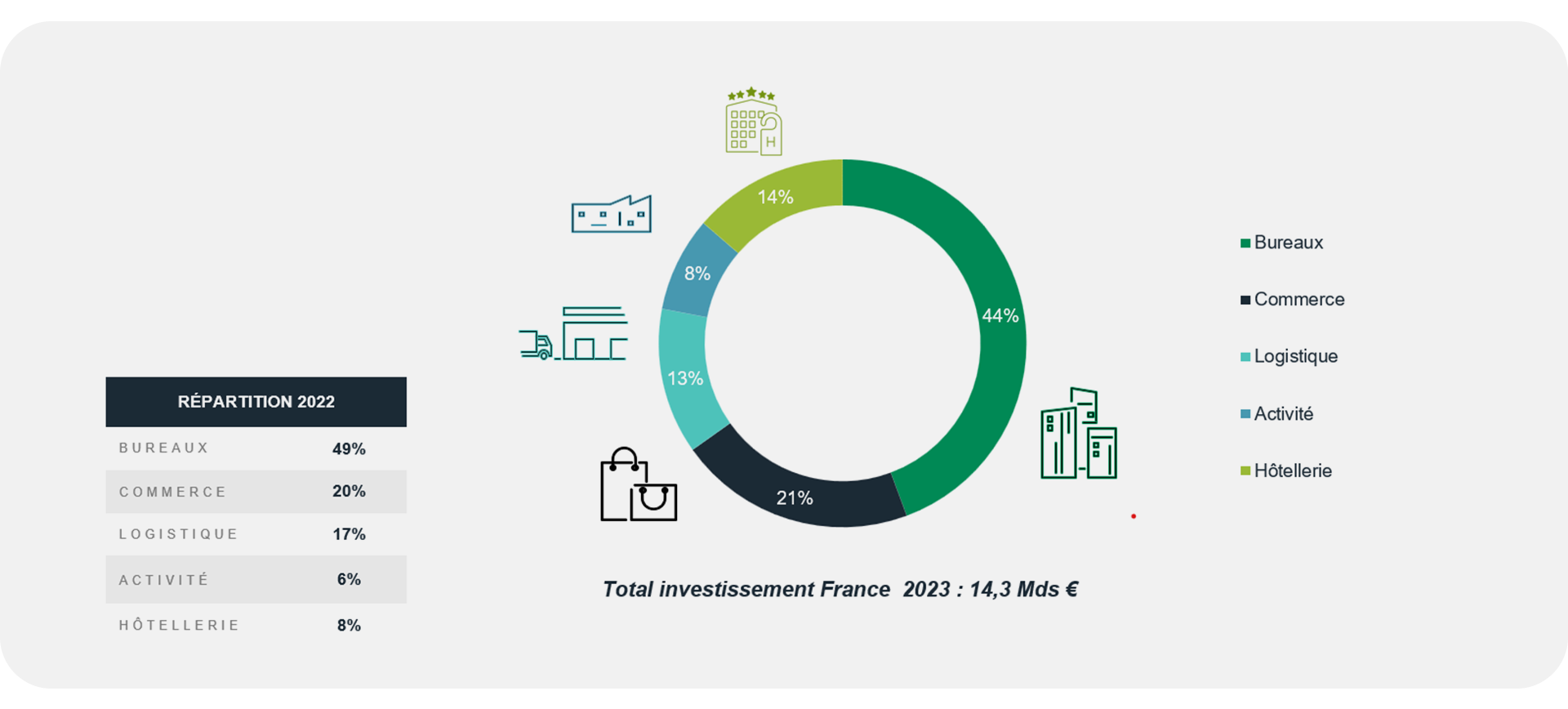

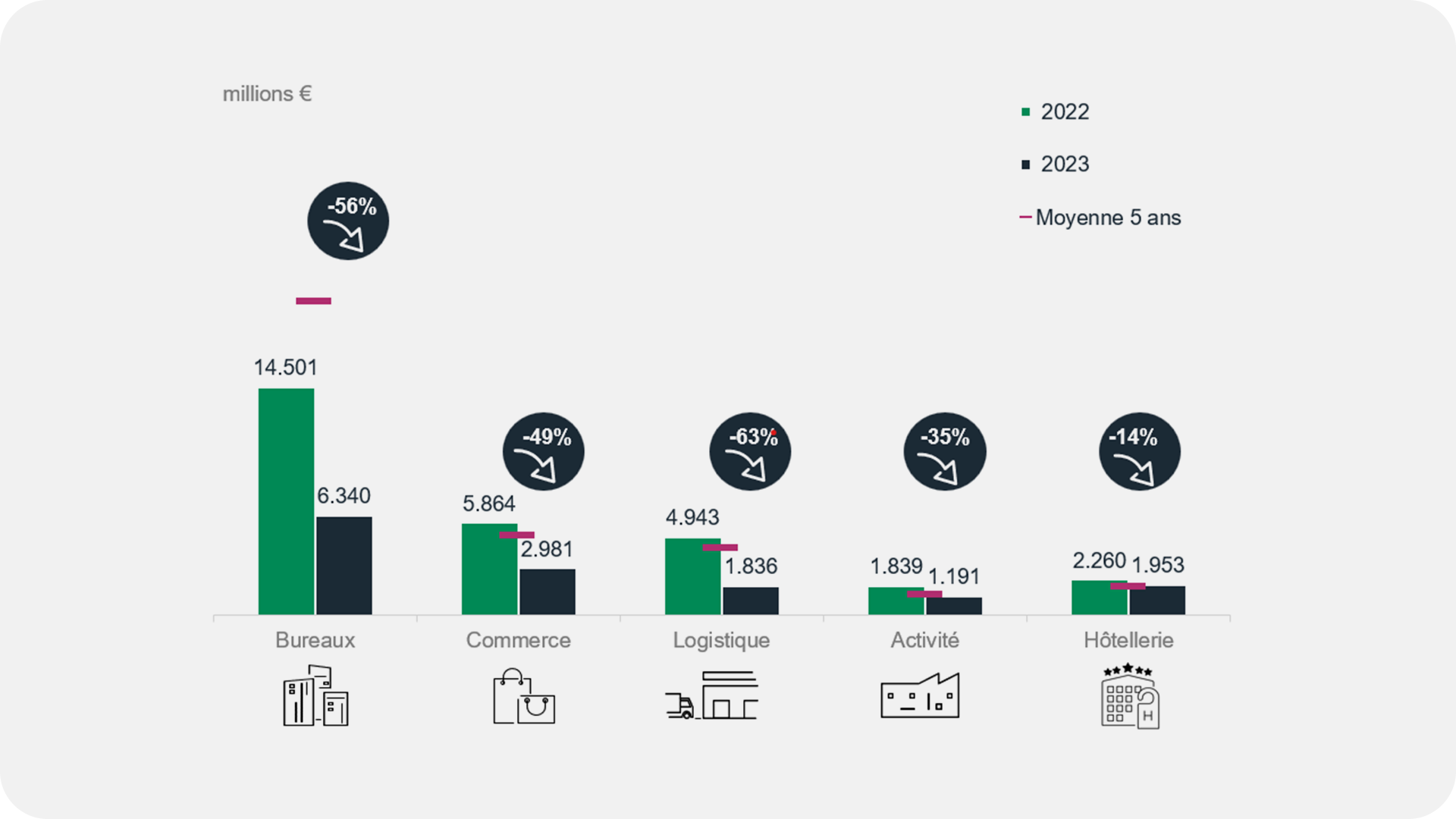

Despite the turbulence in the Office sector, the asset class accounted for 44% of total real estate investments in 2023. Nevertheless, this was a substantial 56% less than the capital invested in the sector in 2022. This drop in capital investment was also witnessed in the Logistics sector, which witnessed a decrease of 63% from 2022 to 2023.

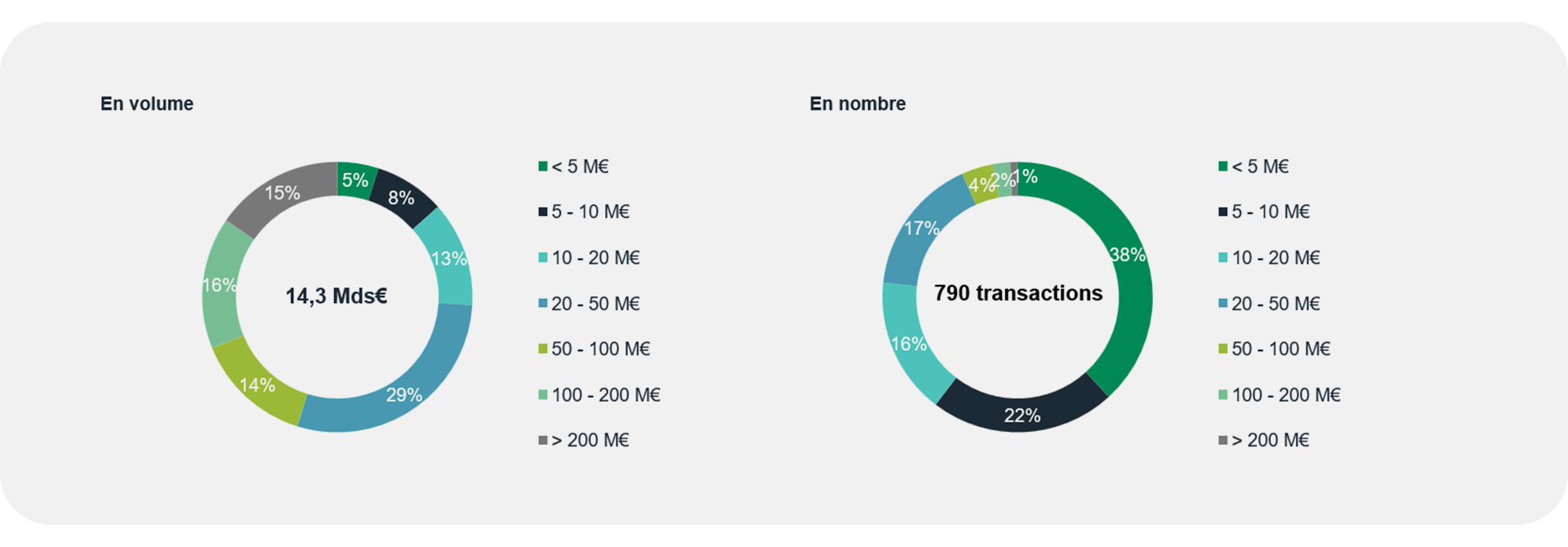

60% of transactions in 2023 were under 10 million euros, and just 3% were over 100 million euros, demonstrating the lack of risk appetite and preference for smaller transactions.

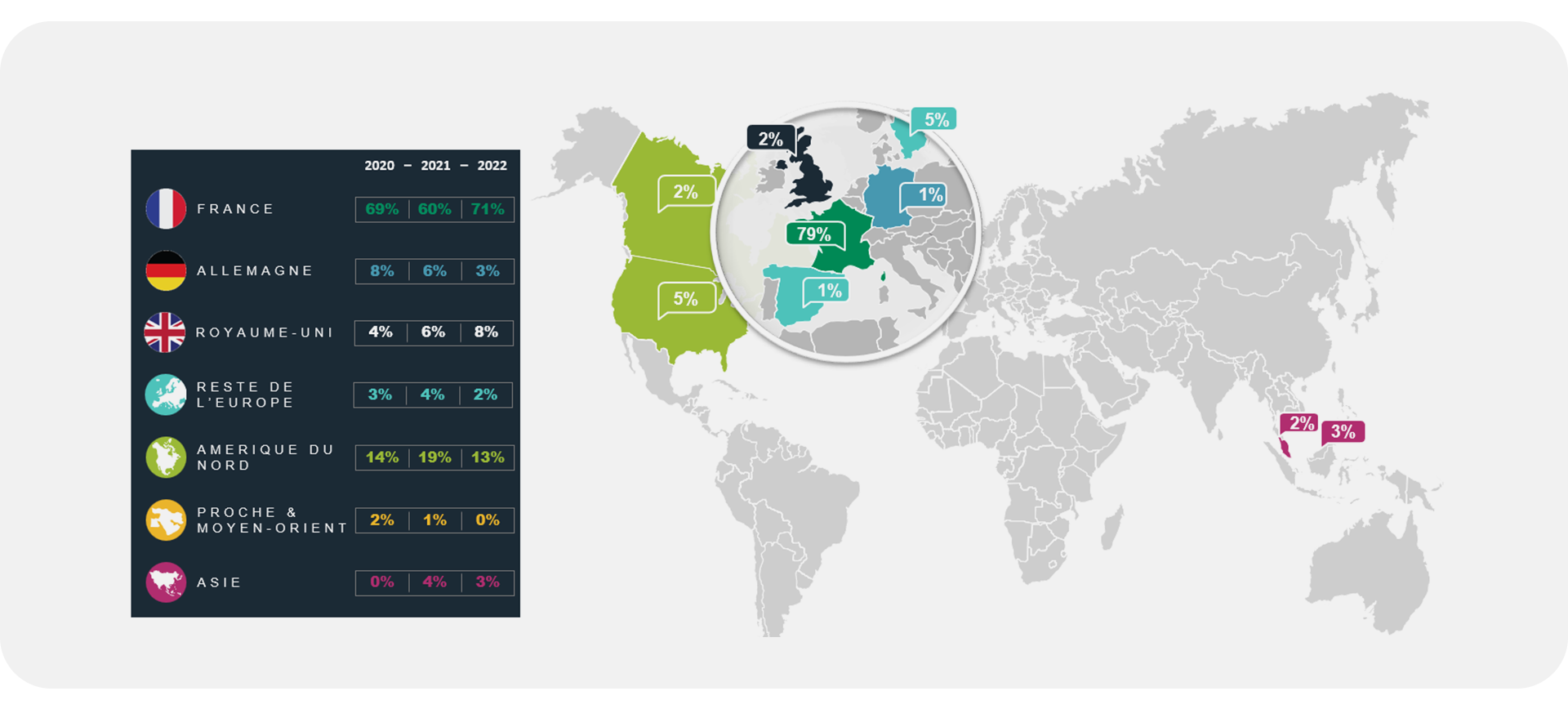

The percentage of domestic capital invested in the French real estate market increased in 2023, accounting for 79% of the total volume, in comparison to just 69% in 2020, 60% in 2021, and 71% in 2022.

The second most active real estate investor in the French market was North America, representing 7% of the total volume in 2023, however a notable drop from its 13% in 2022 and 19% in 2021.

GRI Club will be gathering France’s expert real estate market professionals once again on February 27 for the online meeting: Ressources numériques et data au service de l'asset management.

Read more and register here.

Can France revive itself and face the challenges of 2024? This was the question among real estate investors, lenders, asset managers, and economists gathered at GRI Club’s first economic forum of 2024, Coup d’envoi du marché immobilier 2024, in Paris.

French Market Trends and Macroeconomic Projections

Hélène Baudchon, Deputy Chief Economist at BNP Paribas, began with a keynote address on French market trends and macroeconomic projections.France, similar to the rest of the eurozone, is on the verge of recession with zero to slightly negative growth expected in Q4 2023, and zero to barely positive growth in Q1 2024. A modest recovery is expected from spring, prompted more by household consumption than by companies.

BNP Paribas GDP growth forecasts in developed markets (Image: BNP Paribas Markets360, December 2023)

PMIs (Purchasing Managers' Index) and the ESI (economic sentiment indicator) in the eurozone are slightly encouraging, having both shown recent increases. Meanwhile, recent surveys show mixed sentiments from the French population regarding unemployment prospects, personal finance, standard of living, and chances of making major purchases.

Monthly household survey results in France since 2005 (scaled data) (Image: INSEE, Macrobond, BNP Paribas)The country is experiencing ongoing disinflation, which is expected to continue until falling below the 2% target around summer. This is an important factor supporting growth, as is wage growth, which, although weaker than in 2023, should remain dynamic.

The situation on the labour market is becoming less favourable, although the expected rise in unemployment should remain contained. The substantial rise in defaults also constitutes a significant downside risk to the labour market.

The adverse effects from previous interest rate hikes may not have been fully felt yet. In fact, both negative and positive effects are still to be felt. The expected and observed decreases in central interest rates, which influence long-term interest rates, are already yielding positive results.

Euro Zone Rate with BNPP 2024 forecast (Image: BNP Paribas)

The housing crisis is expected to continue, running the risk of impacting the wider economy. Other challenges faced by the market include ensuring fiscal stability, trade-competitiveness deficit, and transaction volumes.

Commercial Real Estate Investment in France

Olivier Ambrosiali, Deputy General Director of BNP Paribas Real Estate, moderated the Cycle d’Investissement discussion, presenting in-depth data on commercial real estate investment in France over the past years, and more closely in 2023.Last year, France saw a considerably lower level of real estate investment, with a total of approximately 14 billion euros, compared with an annual investment of around 28 to 29 billion euros annually between 2020 and 2022.

History of investments in commercial real estate in France (Image: BNP Paribas Real Estate)

Despite the turbulence in the Office sector, the asset class accounted for 44% of total real estate investments in 2023. Nevertheless, this was a substantial 56% less than the capital invested in the sector in 2022. This drop in capital investment was also witnessed in the Logistics sector, which witnessed a decrease of 63% from 2022 to 2023.

Distribution of investments by asset type in France in 2023 (Image: BNP Paribas Real Estate)

Distribution of investments by asset type in France in 2022 and 2023 (Image: BNP Paribas Real Estate)

60% of transactions in 2023 were under 10 million euros, and just 3% were over 100 million euros, demonstrating the lack of risk appetite and preference for smaller transactions.

French commercial real estate investments by amount in 2023 (Image: BNP Paribas Real Estate)

The percentage of domestic capital invested in the French real estate market increased in 2023, accounting for 79% of the total volume, in comparison to just 69% in 2020, 60% in 2021, and 71% in 2022.

The second most active real estate investor in the French market was North America, representing 7% of the total volume in 2023, however a notable drop from its 13% in 2022 and 19% in 2021.

French commercial real estate investments by nationality in 2023 (Image: BNP Paribas Real Estate)

GRI Club will be gathering France’s expert real estate market professionals once again on February 27 for the online meeting: Ressources numériques et data au service de l'asset management.

Read more and register here.