Divulgação/GRI Club

Divulgação/GRI ClubOpportunities and challenges in Latin America through 2024

June 29, 2023Real Estate

Written by Sarah Garnett

The end of the era of easy money is upon us, and it’s time to start thinking about what that means for investors. The past decade was marked by weak financial systems, deflationary pressures, and massive unemployment - forcing central banks to take hyper-aggressive measures, including zero and negative interest rates, and large-scale bond purchases.But things have changed. The financial systems on both sides of the Atlantic have improved, labor markets are tighter, and regulation has improved to prevent similar issues from arising again. While some structural forces could drive inflation in the coming years, we’re in a more balanced world with some deflationary and inflationary pressures.

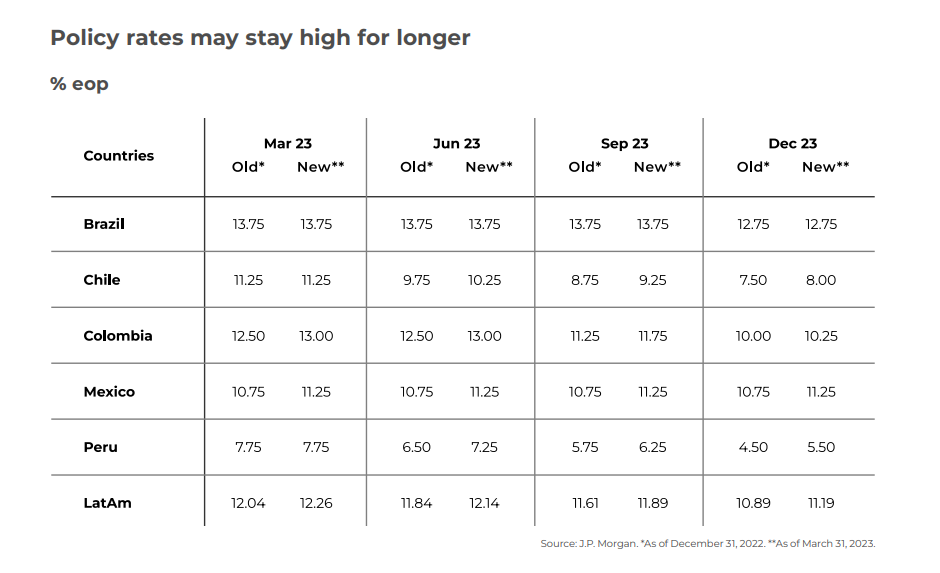

Current policy rates in both Europe and North America are well above what they should be sustained at, and central banks will have to cut at some point. However, market predictions that the Fed will cut rates significantly in the next couple of months is wildly optimistic. The Fed may hike one more time, but they’re likely to hold rates steady for at least three to six months, probably until the end of the year, to see if disinflation takes hold. This means there could be a gradual adjustment to assets that were priced based on the very low interest rates of the last decade. It’s a healthy adjustment to a decade that was truly distorted.

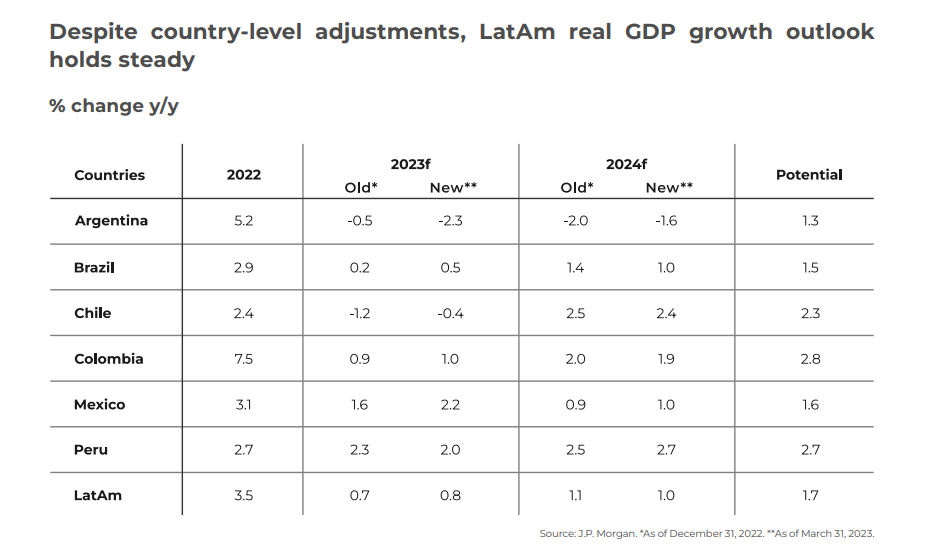

The global economy is currently facing a lot of uncertainty indicating that we are heading towards a slowdown, and the real estate market is not an exception. Although the nominal growth seems reasonable at the moment, real activity is already pretty weak. To prepare for the possibility of a downturn, we need to look at companies and financial systems that are struggling to deal with the total change in the financing landscape.

In Brazil, the interest rate is currently at 14 percent, which poses a challenge to real estate investors looking for mid-teens returns for development. Buying a government bond may seem like an easier way to achieve these returns. However, people continue to invest in real estate because of the inflation-adjusted rents that they receive. But what is the risk premium over the risk-free rate in such investments? These are crucial questions that need to be answered when considering real estate investment in Latin America.

When interest rates are low, below 10 percent, real estate investment returns are easier to produce. However, when they are above 10 percent, it becomes difficult to make a profit. Liquidity in assets is an asset, but it also has a downside, and it is the responsibility of investors to weigh both sides of the coin before making investment decisions.

If the world enters a more volatile interest rate environment with higher term premiums, it can lead to increased funding costs, regardless of the country. Inflation predictability is crucial, and the volatility of inflation can impact long-term yields more than central bank policy rates. If inflation becomes unpredictable, central banks’ balance sheets will decrease, leading to a changing global funding environment.

In recent years, US commercial real estate trends have shifted dramatically. While there has been an oversupply of non-prime locations and commodity Offices, there has been an acceleration of growth in sectors such as Logistics, Data Centres, and Multifamily and Residential markets. Big companies have been leaning towards these sectors for some time and are poised to benefit from them. Despite the current struggles, there are still areas of strength that real estate firms can take advantage of, but the vacation rate for other commercial properties remains high.

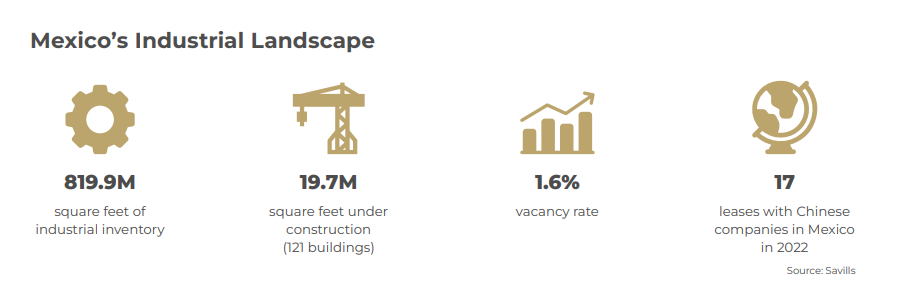

Latin America has a significant advantage in the deglobalization trend because of its geographic location. Investment in supply chains in the region could benefit from loading goods onto ships that can reach deep ports in the United States. This is a long-term project, which could take up to a decade to complete, but it is already yielding results across sectors in Mexico. CEO and CFO surveys show that supply chain resiliency is a consistent concern, meaning that companies want to shorten their supply chains.

In today’s global economy, regionalization and resiliency in supply chains are becoming crucial, especially with recent events like the pandemic that caused disruptions in global supply chains. For data centres and logistics, it’s important to have them close to your population centres to ensure faster and more efficient delivery. This regionalization strategy is already being applied in countries like Mexico, Poland, and Hungary, as they continue to be a greater part of the supply chains of Western Europe.

Nearshoring Opportunities

The upcoming US presidential elections have caused concern and instability, not just for the US but also for its neighbouring countries. While the US construction industry is booming, there are concerns about meeting the capacity to deliver the projects on time. This has created an opportunity for countries in Latin America to become a hub for nearshoring.Nearshoring is not just about moving labor to a new country - it’s about creating a supply chain. The opportunity for countries in Latin America is to get pad-ready sites and to get their government, business community, and utilities on board. It’s all about where is the power, where is the electricity, where is the pad, and where is the port. By doing so, Latin America can also become a major supply chain hub that can provide everything from car manufacturers to chip plants.

Many auto companies have already started operations in Mexico, and now there is a growing interest in expanding nearshoring to other countries in the region. Latin America provides access to skilled workers and has a growing business community, making it an ideal platform for US companies to expand their operations. However, countries must be proactive in creating a supply chain that offers companies everything they need to operate efficiently.

The Future of Data Centres

The growth of Data Centres is only set to increase in the coming years, with experts predicting a 26% growth rate annually until 2027. While Logistics buildings are popular choices for Data Centres, there is also a lot of development occurring in suburban and rural areas. With the rise of cloud computing and the need for more robust Data Centres, it’s clear this asset class is going to play a vital role in the real estate industry in the coming years. As such, investors should consider data centres as a key topic to focus on when it comes to real estate investment.Data Centres present an exciting and profitable investment opportunity, with a bright future ahead. The alluring potential of the sector translates to growing interest, with investors seeking alpha in Brazil and Colombia. Right now, investing in Data Centres promises a return of 15-16% dollars net. Colombia appears to offer investors the best conditions to take advantage of the trend. While Mexico is also an option, given that the country is undergoing a technological revolution, it may not be the best place to invest in hyper-scale projects.

The reasons behind this trend are straightforward: they are essential for companies to store, analyze, and process data, and the growth of AI is making them more critical than ever before. With the rise of usable AI, Data Centers are going to be the main real estate impact from now on.

In recent years, Logistics buildings have become incredibly popular as hosts for these Data Centre projects. With Logistics in every city across North America, they are well-placed to take advantage of proximity to population centres. Additionally, they are usually single-story and flat, making them the perfect hosts.

(Foto: GRI Club)

The Evolution of Offices

With the rise of hybrid work arrangements, Offices are no longer just desks and meeting rooms. As companies embrace the idea of having a balance between remote and in-person work, they are changing their workplace layouts to be more open and to provide common areas such as restaurants, game rooms, and creativity spaces. This shift to Co-living and common amenities has caused an increase in demand for Office space, with companies needing more square footage per employee.Building managers and owners are investing in lifestyle amenities to attract tenants. One example is childcare facilities in Office buildings, which allow employees to have their children nearby during the workday. Similarly, pet centres are becoming more popular, with employees able to bring their pets to work and let them play for the day. These amenities provide not only convenience for employees but also a sense of community and camaraderie in the office.

However, the US currently faces a problem with too much Office space and not enough demand for it. While these lifestyle amenities may attract tenants, it is not the complete solution to the problem.

As the market continues to evolve, it will be important to consider how to repurpose underutilized office space to meet the changing demands of today’s workforce.

Financing & Investments

The Latin American real estate market has great potential for growth and returns on investments, but it’s important to recognize the challenges and the different investment types. Political instability, currency issues, and high inflation rates have been a catalyst for international investors leaving the market, but there is hope for a return with a stable political environment and lower interest rates.When investing in the Latin American real estate market, it’s crucial to have a local partner who understands the market and its trends. With this knowledge, investors can make strategic investments that will see high returns on investments.

While countries like Brazil, Chile, and Mexico offer opportunities, investors need to be comfortable with the currency, and some countries are not yet ready for institutionalizing investments. It’s essential to assess each country individually to determine whether they are ready for investment and have a clear exit strategy. While foreign investors may see Latin America as a distressed market, this is a misconception that needs to be addressed.

The Rise of Private Credit

Private credit is becoming a major force in financing, poised for explosive growth across all corporations in the coming years. Traditional banks, especially regional ones, are seeing a retrenchment in lending, opening up a void for private credit to step in. This shift is not specific to real estate or any one industry, but rather a structural trend that will revolutionize the way that corporations are financed.Policymakers are recognizing the benefits of private credit, which offer a safer alternative to regional banks that often lend long-term to risky ventures. Businesses are also recognizing the advantages of private credit, which offers a better match for seven-to-ten-year loans.

Additionally, private credit is not necessarily more expensive. Rates will depend on individual circumstances, but there will be funding available for decent assets. It will be harder for distressed sellers, but good assets with positive net operating income growth, rental growth, occupancy, and low vacancy will still find financing.

The private credit industry will step in to any financing opportunities, and the financial sector will evolve enormously as a result. Overall, this shift in financing represents a natural progression of the financial sector and will be of great benefit to all.

If investors want projects with a long-term view, perpetual products are an excellent choice, meaning that investors do not have to worry about their money being returned in a short period. With assets like Logistics, Data Centers, and a significant investment in Multifamily residential units, investors can expect a stable return on investment over the long-term.

While the world is still working out the costs of fragility that come with fractional reserve banking, private credit seems to be a better match between liabilities and assets and the time horizon.

The correlation of bond yields in Latin America with those of the West is a factor that could contribute to capital flowing into the region. Long-term assets have high funding costs, especially bonds that mature in over five to seven years.

Additionally, if yields remain high in the region while they fall in the West, capital could start to flow into Latin America. However, this is a speculative possibility, as it also depends on stability in both political and policy environments.

Investments in Brazil: Opportunities and Caution

Brazil has its ups and downs as an investment destination. The non-deliverable currency of Brazil makes it a challenging place for investors to hedge their investments. Unfortunately, this should not come as a surprise because returns on investments in dollars have been underwhelming. However, on the bright side, investors can expect better returns if they opt to invest in BRL. The next 15 years remain uncertain, and the suggestion is to exercise caution when investing in Brazil.According to the speakers, there is limited demand from global investors for Brazil. This is mainly due to the return on investment being affected by currency exchange rates. The speakers noted that local investors would be more interested in certain asset classes that offer decent returns, particularly in specialized opportunities and credit. It is important to show good experiences to the investors to attract them to invest.

Investments in Mexico: Opportunities and Growth On the other hand, investments in Mexico offer potential opportunities. With the ongoing conflict between the US and China and other political global events, Mexico is in a unique position for growth. The following 15 years are anticipated to be much better than the previous 15, even with the North American Free Trade Agreement (NAFTA) no longer in effect.

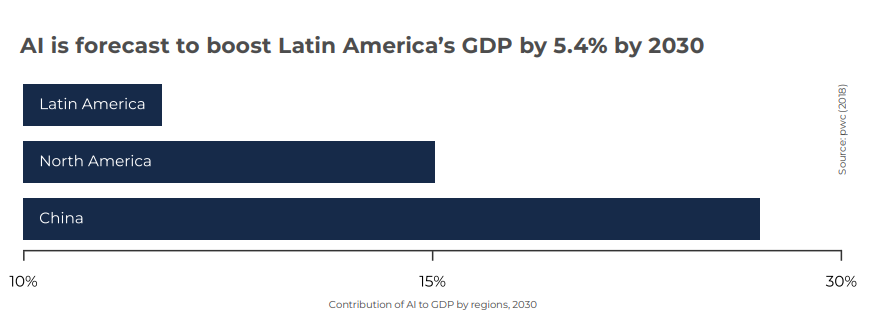

In 2015, the currency appreciated by 15-20%, something that has not been seen in 50 years. One of the unique opportunities that investors are facing is the current trend towards sustainable investments. ESG initiatives and having an internal ESG team are imperative for investors to keep up to date with investor demands, and for unique investments to thrive.

Industrial investment options seem to be the most viable right now due to the robust growth of the sector. However, resorts and real estate financing are also potential avenues worth exploring. According to recent data, resort investors are enjoying a healthy return on investment, with some reporting north of 20%.

The Future of Investment in Latin America

The speakers were asked if they wished they had invested more or less in the region over the past 15 years and how they think the next 15 years would compare with the past 15 years. They agreed that their countries would always be seen as opportunistic, which attracts certain investors during down cycles of mature economies such as the US and Europe. However, they would love to have more stable investors instead of those who come in and out.They commented that it has taken a lot of time for most of the Latin American countries to get to the point where they have potential like Chile, which is well-structured. They expect that most countries in the region will still struggle with attracting local and foreign investors, with ups and downs, in the next 15 years.

Selling large assets worth over $100 million in Latin America can be a daunting task due to liquidity issues. Finding people who can stroke a $150 or $200 million check is becoming increasingly difficult.

Technology & Innovation: a new cycle

It is no news that the pandemic and lockdown had a significant impact on various sectors, including the PropTech industryInvestors often overlook the long-term benefits of innovation, as they are focused on shortterm gains. It is crucial for real estate companies to not make the same mistake when it comes to incorporating technology and innovation. PropTech is an industry that has seen great benefits from innovation and investment, and companies should not hesitate to take advantage of the opportunities available. By investing in innovation, companies can stay ahead of the curve and better adapt to the ever-changing market.

One of the key factors that will drive the new cycle in PropTech investments is the increasing demand for technology in the real estate industry. While the industry has traditionally been slow to adopt new technologies, the pandemic has forced many companies to reconsider their strategies and look for ways to adapt to changing market conditions. As a result, we are seeing a growing number of real estate companies investing in new technologies that can help them operate more efficiently and effectively.

Another important factor driving the new cycle in PropTech investments is the increasing innovation we are seeing in the space. Over the past few years, we have seen a wave of new startups and technologies emerge in the real estate industry, each with the potential to disrupt traditional business models and create new opportunities for investors. From virtual reality and blockchain to data analytics and machine learning, there are countless innovative technologies that are reshaping the way companies think about real estate.

Finally, the third factor driving the new cycle in PropTech investments is the long-term growth potential of the industry. Despite the short-term disruptions caused by the pandemic, the real estate industry remains one of the largest and most important asset classes in the world. In fact, many experts expect the industry to continue growing over the coming decades as populations continue to grow and urbanization increases. As such, there is no shortage of opportunities for investors in PropTech, and is expected to see continued growth and innovation in the years to come.

Government Support and Regulations

Another factor driving the new cycle of PropTech investments is the increase in government support and regulations. Governments are now interested in supporting and promoting technology in the real estate industry. This support will create a conducive environment for PropTech companies to develop and thrive. Additionally, regulations will increase transparency and accountability, which will attract more investors to the industry.The Use of AI in the Industry

One of the most significant disruptors in the industry is Artificial Intelligence (AI). AI is a powerful tool that is already being used by many companies to streamline their operations and increase efficiency. However, the adoption of AI has been slow, and many businesses are struggling to keep up with the pace of change.For those that are willing to embrace this new technology, the rewards can be significant. AI can be used for a wide range of tasks, from data analysis to estimating costs. However, there are also concerns about the potential risks of AI, and how it could be used to replace human workers. As such, it’s essential that companies take a cautious and considered approach to the adoption of AI, to ensure that it is used ethically and responsibly.

The potential of AI as a research tool is almost limitless. With AI like Chat GPT, companies can access vast amounts of research data from multiple sources quickly and easily. This can save businesses months of research time and simplify the building of a business plan.

One example of using AI to improve business growth is by finding the right price for products that have no equivalent in the market. This is where Chat GPT can come in handy, helping businesses discover the right price point.

The acceleration of ESG in Business

Environmental sustainability is becoming increasingly important in investing. Many companies now have a policy that they will only invest in developments that are carbon zero. Not only does this help the environment, but it also ties into the overall social responsibility of the investment. As investors, it is also important to consider the potential for distress cycles, particularly with regards to leverage in the market.ESG practices are a requirement to meet the demands of investors and consumers. This is especially true for large, multinational corporations such as Microsoft, Amazon, and Google, who are demanding ESG practices from their business partners. However, implementing ESG practices in the real world is not always straightforward.

While some businesses have strong governance and environmental practices, social issues can be more challenging. Despite this, companies must address ESG requirements as part of their agenda to stay competitive and maintain their reputation.

Governance is an integral part of ESG practices and must be in place to create a framework for environmental and social efforts. Without proper governance, businesses may not be able to implement the necessary changes to create sustainable practices.

(Foto: GRI Club)