GRI Club

GRI Club The Future of Europe’s Real Estate Asset Classes with WIRE

Women in real estate meeting in London give insights into the alternative asset classes such as Life Sciences and Data Centres

March 7, 2023Real Estate

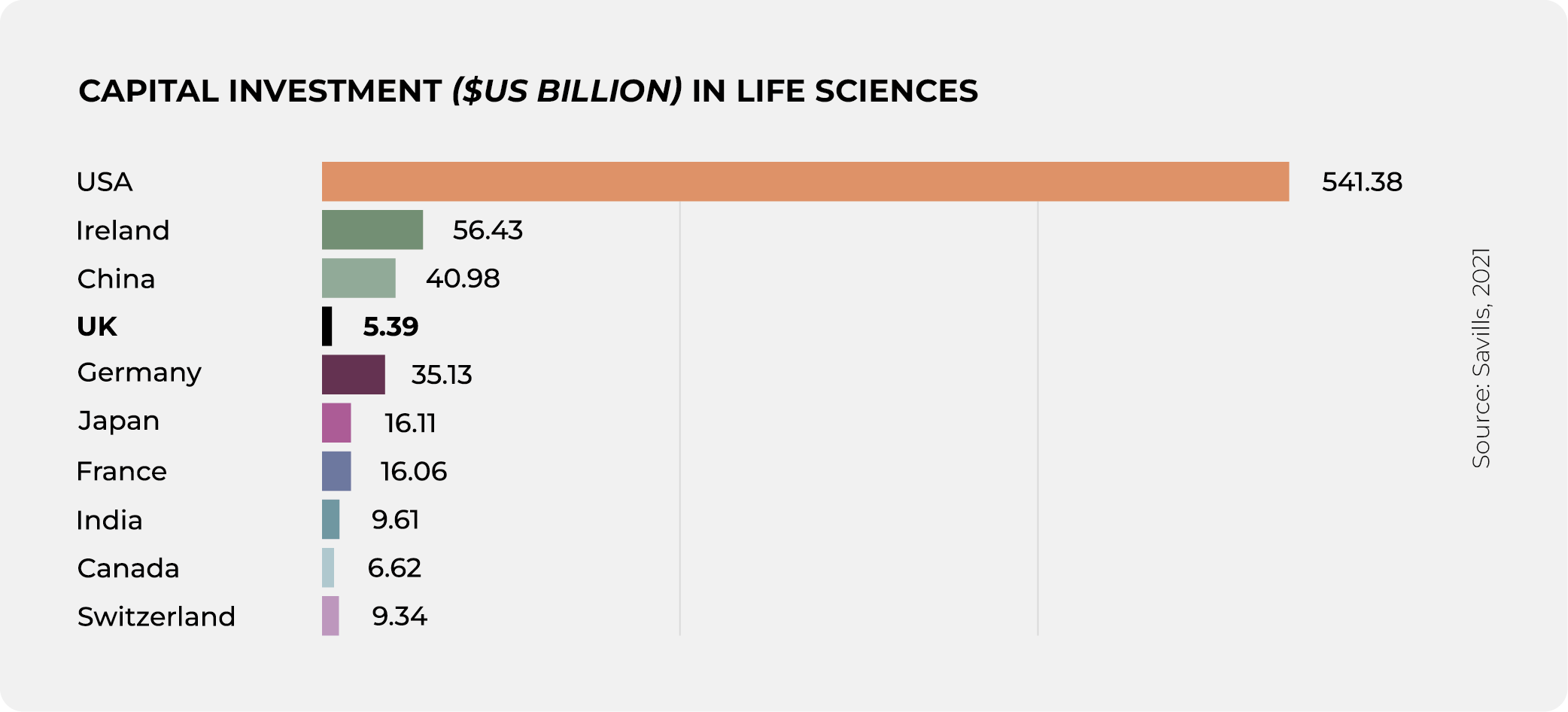

Life Sciences: A beacon of hope for the UK?

Life Sciences in the UK were noted to still be in the beginning stages of growth, with significant investment required for the industry to flourish. The country’s GDP levels are not strong enough to attract the sector - in 2022, the UK was the only country in the Eurozone to have negative GDP growth. However, just at the end of last year, Kadans and Canary Wharf Group announced the largest Life Sciences project to date in central London.

Investment firm KKR names it as one of their favoured sectors in 2023, and a takeaway from the GRI club meeting was that the UK has appeal and the main building blocks for this area to grow. The cycle is just starting for this asset class.

The UK government has also committed to backing Life Sciences, in 2022 providing £260m for manufacturing. However, the UK’s tax rates were claimed as the reason for AstraZeneca’s move of a $400m project to Ireland recently. Some have claimed that the UK is falling behind despite excellent Research & Development infrastructure and expertise in genomics and AI. According to GRI club members, inward investment needs to increase to keep companies in the country.

The UK is overall in a good position to create an investment pipeline, but this kind of consistent funding is needed to progress. Government announcements of support encourage long-term investment ambitions, but club meeting attendees say that escalating construction costs are further motivating companies to move to the USA; Ayming’s UK Innovation Barometer revealed that 69% of businesses have moved R&D activity abroad in 2022 and that 70% are planning to do so in 2023.

Life Sciences are not exempt from the age-old asset class problems of competing with London, as well as finding talent and investors. Executives say that companies can be seen moving to the USA for property values; however, staffing costs and wages are higher in the USA, so ultimately the fight for UK dominance comes down to people vs property values.

The UK government has also committed to backing Life Sciences, in 2022 providing £260m for manufacturing. However, the UK’s tax rates were claimed as the reason for AstraZeneca’s move of a $400m project to Ireland recently. Some have claimed that the UK is falling behind despite excellent Research & Development infrastructure and expertise in genomics and AI. According to GRI club members, inward investment needs to increase to keep companies in the country.

The UK is overall in a good position to create an investment pipeline, but this kind of consistent funding is needed to progress. Government announcements of support encourage long-term investment ambitions, but club meeting attendees say that escalating construction costs are further motivating companies to move to the USA; Ayming’s UK Innovation Barometer revealed that 69% of businesses have moved R&D activity abroad in 2022 and that 70% are planning to do so in 2023.

Life Sciences are not exempt from the age-old asset class problems of competing with London, as well as finding talent and investors. Executives say that companies can be seen moving to the USA for property values; however, staffing costs and wages are higher in the USA, so ultimately the fight for UK dominance comes down to people vs property values.

Data Centres: a post-COVID dream?

Data centres flew under the radar pre-pandemic, but after the arrival of WFH - which according to executives at the GRI Chairmen’s Retreat this year is here to stay - and with the reconsideration of ESG and environmental impact on decision-making, countries are looking further into the nature and density of this alternative investment.

Europe sees the market growing in many cities, with Frankfurt, London, Amsterdam, Paris, and Dublin as mainstays on Cushman & Wakefield’s European region list and other markets in Zurich, Madrid, Stockholm, and Berlin receiving more interest. Europe stands out for its focus on sustainability and political stability as well as tax incentives.

Europe sees the market growing in many cities, with Frankfurt, London, Amsterdam, Paris, and Dublin as mainstays on Cushman & Wakefield’s European region list and other markets in Zurich, Madrid, Stockholm, and Berlin receiving more interest. Europe stands out for its focus on sustainability and political stability as well as tax incentives.

Executives at the GRI Women in Real Estate conference

Executives at the GRI Women in Real Estate conference

In the last month, data centre firm Datum announced plans to open new sites in Farnborough and Manchester. Before that, Vantage Data Centers entered the London market with the development of a £500m campus.

In the UK, there are concerns about caps on Data Centre property; additionally, data centres suffer during times of high energy costs such as last year’s, and there are concerns about meeting ESG goals with the vast amounts of energy that such constructions use. Data centres are also particularly vulnerable to changing interest rates, with investors in the USA being more selective in recent months and prioritising strategy and the best potential risk-adjusted returns.

In the UK, there are concerns about caps on Data Centre property; additionally, data centres suffer during times of high energy costs such as last year’s, and there are concerns about meeting ESG goals with the vast amounts of energy that such constructions use. Data centres are also particularly vulnerable to changing interest rates, with investors in the USA being more selective in recent months and prioritising strategy and the best potential risk-adjusted returns.

- Security risks are a concern frequently reported on for this asset class. The physical side of data centre security has also been highlighted as a high priority, such as reliable volumetric detection.

- TikTok has been seeking to assure regulators that users' personal data cannot be accessed and its content cannot be manipulated by China's Communist Party, so will open two more data centres in Europe.

- Read Digital Journal’s Data Centre Security Market Report 2023-2030.

One of the industry’s biggest challenges is the physical power delivery of property per square meter. There is a lack of land to fit the requirements of power for data centres, with many of the best locations already being used.

Environmental, Social and Governance

The Women in Real Estate attendees affirm that the industry has a strengthened view of responsibility when it comes to ESG, sustainable investing and obtaining renewable power sources, so the industry is innovating to address these concerns. Nuclear energy was mentioned as a potential solution with the need for development.

Life Sciences is seeing a similar movement with the examination of their power footprint; the UK has advanced to make a clean energy footprint in manufacturing, with a huge step in recent years for renewables. Last year, 40% of the UK’s energy was made up of solar, wind, biomass and hydropower.

Life Sciences is seeing a similar movement with the examination of their power footprint; the UK has advanced to make a clean energy footprint in manufacturing, with a huge step in recent years for renewables. Last year, 40% of the UK’s energy was made up of solar, wind, biomass and hydropower.

Co-Living: the next big asset class for investment?

Co-Living proved a popular asset class at the WIRE club meeting and the UK & Europe Reunion all over Europe. GRI has already taken note of the trend; on the 2nd of March, Spain saw a club meeting on the subject held in conjunction with Greystar at their BeCasa accommodation in Madrid.

Co-Living is by no means a new concept but has exploded in the last decade, with the biggest booms in Berlin. This asset class is evolving while exasperated by affordability challenges for many in Europe. Buildings with this concept can be seen for the elderly, bridging the gap between independent living and nursing care, such as Korian’s recent developments in Germany; otherwise, they are usually advertised to those who want to enjoy convenient, stress-free living at affordable prices. The spaces are even attractive to those on mid-level incomes.

24 major cities accounted for approx 25% of Europe's co-living market value, with 40% of that focused in just two places, London and Amsterdam.

Recent deals in the Co-Living space include:

- M&G’s purchase of a second asset in Dublin for €99.5m, adding to its €75m maiden acquisition in Finland. The Dublin development will offer 148 high-quality homes and communal amenities such as a gym, rooftop gardens, bicycle spaces, balconies and terraces.

- Last year in Spain, 5,000 new beds were added to the market.

- In mainland Europe, co-living spaces can be found in development as far as Bulgaria, where Semkovo is developing a community-owned space converted from a hotel aimed at digital nomads.

There are long-term institutional investor profiles in the space with banks starting to take notice and European real estate fund Patron Capital that bought Vanguard Student Housing, the student co-living manager.

UK & Europe Reunion attendees also remarked that many countries do not have institutional products available for capital to access and that it is a difficult project to scale; on the other hand, Co-Living has a stabilising long-stay factor compared to asset classes such as hotels, and attendees feel confident about the level of risk.

UK & Europe Reunion attendees also remarked that many countries do not have institutional products available for capital to access and that it is a difficult project to scale; on the other hand, Co-Living has a stabilising long-stay factor compared to asset classes such as hotels, and attendees feel confident about the level of risk.

Representing women in real estate; mentorship and resilience

Audrey Klein at the Women in Real Estate club meeting, discussing growing asset classes

Overall, the attendees noted that there are long-term institutional investors in the space, and

the demand and occupational strength of these asset classes will remain strong through the current pricing shifts which will see new normals across the board. The ability to grow rents for these sectors also makes them attractive.

Some attendees of the event included:

- Kimberly Hourihan, Global Chief Investment Officer at CBRE

- Amy Daniell, Director, Hyperscale Team - Global Data Center (EMEA), from NTT Data

- Audrey Klein, Non-Executive Board Member - Chair of ESG Committee at SFO Capital Partners and Planet Smart City

- Claire Dawe, Head of Asset Management at Stanhope

- Ellen Langdon, Asset Manager from SVP Investments & Acquisitions

- Jenny Gardner, Development & Construction Director at ARC

- Jill Xiaozhou Ju, Founder and CEO of True North Management

- Kasia Averall, Head of Cluster Development from Cell and Gene Therapy Catapult

Audrey Klein, the Chair of the ESG Committee at SFO Capital Partners and Planet Smart City and one of the moderators at the club meeting, says that her advice for women in real estate is to be strategic and have a five-year plan while trying to find sponsors within your own organisation. “Women often think that if they just work hard that they'll get noticed. You know, you don't get noticed. Like, I mean, you do, but nothing really happens unless you make it happen.”

On WIRE, she also expressed that “it's supposed to be a place where you can network and find ways of creating career growth, doing deals and making things happen amongst women. You know, because men make things happen amongst themselves all the time.”

WIRE, the industry partner of the club meeting, is a growing force in the industry and an opportunity for women to receive indirect mentoring and make connections with one another.

For more formal mentoring, WIRE associates with Mentoring Circle, which provides this opportunity for junior female property professionals.

Another significant conclusion on women’s position in the industry was that this demographic is more affected by the current work-from-home wave, as it is more difficult to build relationships over online meetings than in-person, and these relationships are key for success.

Ultimately, the best answer is to do business together - it's how we advance women and differentiate ourselves.

Women in Real Estate will gather again at Europe GRI 2023.

Written by Sarah Garnett

On WIRE, she also expressed that “it's supposed to be a place where you can network and find ways of creating career growth, doing deals and making things happen amongst women. You know, because men make things happen amongst themselves all the time.”

WIRE, the industry partner of the club meeting, is a growing force in the industry and an opportunity for women to receive indirect mentoring and make connections with one another.

For more formal mentoring, WIRE associates with Mentoring Circle, which provides this opportunity for junior female property professionals.

Another significant conclusion on women’s position in the industry was that this demographic is more affected by the current work-from-home wave, as it is more difficult to build relationships over online meetings than in-person, and these relationships are key for success.

Ultimately, the best answer is to do business together - it's how we advance women and differentiate ourselves.

Women in Real Estate will gather again at Europe GRI 2023.

Written by Sarah Garnett